Written by Vaibhav Saxena

Valuing life with a climate change countering motto ‘save our planet’ ambitions remain on top priority for the world, enabling action at COP29 hosted by Baku for 2024.

COP29 President-Designate letter describes the 2024 UN Climate Change Conference in Azerbaijan as “a litmus test” for the Paris Agreement, global climate action, and cooperation, with a new collective quantified goal (NCQG) on climate finance as its “centerpiece” with an active engagement of global, regional, national, and subnational groups by adopting an advanced “holistic view” of sustainable development with an exclusive process that delivers inclusive outcomes. At COP29, the participating countries will be further reporting on their respective actions post COP28 and reaffirming their commitments towards climate change objectives while exploring opportunities.

Diversified Partnering Options

Vietnam signed the Just Energy Transition Partnership (JETP) on 14 December 2022 with G7 countries and as it maintains momentum, there are challenges pertaining to mobilization stream when it gets elevated considering economic instability posed to due fluctuating global economic and security dynamics.

On one hand, Vietnam focusses on integrating the local industry as a trend towards its Industrial Revolution 4.0, while modernising and digitalising the power systems and networks by embracing smart technologies. In its green journey the country acknowledges and emphasize on the importance of integrating renewable energy sources such as wind, solar, and hydropower when in parallel it promotes its energy security with other sources of electricity generation.

On the other hand, financing remains a riddle that is yet to be solved. Although, international commitments, green funds, bonds, and credit sources are in abundance to ensure a sustainable energy transition, but bankability consistently strikes as a boulder to support non-recourse financing instruments that highly rely on leveraging risks among the international players. On the investment front, mainly, there are two options for Vietnam to realise its planned targets under the Power Development Plan VIII for 2021-2030, with a vision to 2050 (PDP-8), one option being public-private partnerships which is seen to be more suitable for large-scale projects and this way invites participation of the state-owned enterprises, while the other option is through the Investment Law that supports private independent power producers.

Vietnam’s Policy Movements and Regulatory Restructuring

There has been progress made by Vietnam on the policy formulation since the last reporting at COP28 and which is evident from the release of the PDP-8 Implementation Plan in April 2024 and thereafter the much awaited regulatory framework for the Direct Power Purchase Agreement (DPPA) mechanism that entered in effect from July 2024 and rooftop solar specific regulation in October to address unresolved matters hindering smooth development of self-produced and self-consumed rooftop solar power sources throughout the country. However, there is surely more focused approach required to match with the global pace and for which the work is in progress to ensure a higher economic performance for 2026 evaluation of the current government. Further, the country is determined to reaffirm its commitments at the COP29 in November 2024.

Planned Generation Capacities under the PDP-8 Implementation Plan

It is pertinent that the PDP-8 Implementation Plan sets out ambitious targets for 2030 to support a diversified energy mix for Vietnam when the focal point remains to boost investments while securing its energy needs in the long run, the electricity generation capacities planned from various sources are as below:

|

Source |

Total Capacity (MW) |

|

Prioritised |

|

|

Domestic Gas |

14,930 |

|

LNG |

22,400 |

|

Coal |

30,127 |

|

Co-generation (residual heat and flue gas) |

2,700 |

|

Hydropower (medium and large) |

29,346 |

|

Pumped storage hydropower |

2,400 |

|

Renewable Energy (RE) |

|

|

Offshore Wind |

6,000 |

|

Onshore Wind (incl. nearshore) |

21,880 |

|

Small Hydro |

29,346 |

|

Biomass |

1,088 |

|

Waste-to-Energy |

1,182 |

|

Rooftop Solar (off grid) |

2,600 |

|

Battery Storage (hybrid |

300 |

|

Other |

|

|

Flexible |

300 |

|

Import (Laos) |

5,000 increase up to 8,000 |

|

RE Export (central and south) |

5,000 – 10,000 |

|

RE to produce Hydrogen, Green Ammonia for domestic and export |

Up to 5,000 (mainly offshore wind source) |

It is ought to be noted that the above stated capacities are under re-consideration in accordance with the Planning Law and accordingly, PDP-8 is expected to see some shifts in target capacities allocation to make sure that the targeted goals are duly achieved within the planned timeframe. In contrast a noteworthy concern persists in relation to the strict timeline i.e. by 2030, leaving the industry and the government with around 6 years to fulfill accomplishments.

DPPA

In order to support the PDP-8 the government of Vietnam had passed Decree 80 in July 2024, laying down regulations on direct electricity trading mechanism between renewable energy generators and large electricity users. Decree 80 is applied to the renewable energy generation units comprising different sources, namely, solar, wind, small hydro, biomass, geothermal, tidal… and rooftop solar systems with electricity operation license as applicable based on the source generation capacity or an exemption from the same as per the existing regulations laid under Circular 21/2020 of the Ministry of Industry and Trade (MoIT).

Decree 80 provides for the following two options:

- Private line sale and purchase of power among RE generation units and large electricity consumers. In this option the power purchase agreement (PPA) price could be mutually agreed among the generator and the consumer. Except where the generation unit performs retail as well, combining power purchase from the national grid and on-site for retail, here, pricing shall be as per the MoIT release.

- Sale and purchase of power through the national grid includes the below:

- Grid connected solar and wind generation units with a capacity of 10MW and above, participating in competitive wholesale electricity market (Trading cycle – 30 minutes each, per trading day). In here that transmission loss is recognized and the payment cycle is 1 month (on the electricity market), from 1st day of each month.

- Industrial consumers buying power from Vietnam Electricity (EVN)/retailers with connection voltage level being 22kV or above, with an output of 200,000 kWh/month (average on preceding 12 months);

- Power retailers in zones, clusters authorized by large consumers for production purposes, buying electricity from EVN through a forward contract with the RE generation units.

In addition to detailing on the power generation and sale models, Decree 80 appendices provide templates for Model PPAs applied for the option no.2 stated above. The said templates mention on renewable energy certificates (REC’s) and carbon credits for which Vietnam has a plan to initiate a pilot program that will transition to formulation of a full-fledged market in the upcoming years.

Rooftop Solar for Self-produced and Self-consumed

Supporting the green transition, the government of Vietnam released Decree No. 135/2024 on 22 October 2024 (“Decree 135”) laying down regulations to encourage the development of self-produced and self-consumed rooftop solar power was initialed, effective.

Categories

Rooftop solar power sources (“RTS Sources”) are divided into two main criteria’s i.e.

(a) RTS Sources connected to the national grid (hybrid sources supplying electricity on-site or at discretion surplus supply to the national grid), development of such RTS Sources shall be less than or equal to the total installed capacity of the existing load and consistent with past 12 months of electricity consumption.

Prior to installing such RTS Sources having capacity of less than 1MW, a notice from the investor, developer/user need to be sent together with the design documents to the provincial construction, fire prevention and fighting, local electricity unit and the Department of Industry and Trade (DoIT) for monitoring.

Grid connected RTS sources should obtain certification from the competent authority being the provincial DoIT.

(b) RTS Sources not connected to the national grid (private power generation for either self-consumption or sale behind the meter). Such RTS Sources are not required registration as per Decree 135, however, a notice from the investor, developer/user need to be sent together with the design documents to the provincial construction, fire prevention and fighting, local electricity unit and the DoIT for monitoring. It further promotes uncapped generation capacity development for such sources.

Capacities of such RTS Sources connected to the national grid shall adhere to the approved thresholds under the PDP8 (including its implementation plan, as to be revised), excluding RTS Sources in island districts and communes having grid but not integrated with the national power system. It further bans import of used PV panels and DC to AC convertors to develop such sources.

Grid connected RTS sources willing to pump surplus electricity to the national grid, with the installed capacity from 100 kW or above, to negotiate mutually and agree on the equipment for collection, monitoring and control system to ensure grid safety.

Incentives for RTS Sources

- RTS Sources not connected to the national grid are prioritized with uncapped capacities while being exempt from electricity operation license. Further, grid connected RTS Sources equipped with anti-backflow are prioritized without any capacity cap.

- Surplus electricity from RTS Sources having capacity ≥1MW are subject to electricity operation license.

- Land repurposing is not inclined for development. For constructions identified as public assets, the RTS Sources shall be treated as technological equipment attached to construction works.

- Energy storage is permitted, paving way for BESS while ensuring administrative ease.

- Grid connected RTS Sources falling within the PDP8 approved capacities, with less than 100 kW can pump surplus power to the grid, but not exceeding 20% of the actual installed and registered capacity, to receive payments from Vietnam Electricity (EVN) at a price equal to the average electricity market price in the previous year. Including such RTS Sources installed on public property, not purchasing or selling surplus electricity.

- Households are exempt from any adjustments to their relevant licenses.

PPA Term

Power Purchase Agreement term for surplus electricity trading from RTS Sources is limited to five (05) years initially, from the commercial operation date of the RTS Source, and is subject to extension upon mutual agreement among the signing parties, in accordance with the then effective regulations.

Transitional Provisions

Investors whose RTS Sources are operational prior to 01 January 2021 are not permitted to connect or register to install additional RTS Sources at the same location.

Whereas, for the households, individuals and public offices those who have developed RTS Sources from 1 January 2021 are required to notify to the DoIT for the purpose of recording the capacity and coordinates.

Restructuring of State-Owned Enterprises

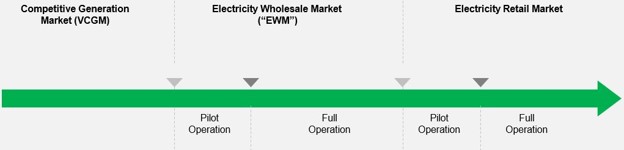

In August 2024, the National Load Dispatch Center (A0) departed from EVN Group umbrella and sparked a new balanced beginning as the National Power System and Market Operation LLC (NSMO) with the MoIT, while the Commission for Management of State Capital at Enterprises (CMSC) maintains supervision. This restructuring is a critical for Vietnam to support the roadmap for its electricity market development plans originating from December 2013, which is planned in a phased manner as follows:

It is true that the plans have been severely delayed due to several economic, political and security variations that not only relates solely to Vietnam but worldwide and it is not the only country which is impacted by the same but this has been witnessed as a global trend when the countries are reassessing their policy transition visions to cope up with the market swings.

Stability Sustainability Suitability

Battery Energy Storage System (BESS)

Decision 1009/2023 of the Prime Minister allowed Vietnam Electricity (EVN) for a pilot BESS project of 50MW. The said pilot project aims to explore ancillary services and inform pricing design and technical standards. The pilot BESS project is proposed to be installed at a substation in the North of Vietnam, serving two functions: peak shifting and frequency control.

The proposed project is an initiative designed for public benefit, assigning EVN for implementation and during the implementation of the said pilot project the country plans to have an on ground experience to base its policy formulation prior to commercializing BESS.

Electricity Law Amendment and Prospective Developments

In parallel to the above stated, the Electricity Law amendment is on the cards and is expected to be passed in 2025 by the National Assembly.

Certainly, Vietnam stands committed to speed up its policy and regulatory framework movements together with the support from the international partners and the industry and hopefully we will see a positive path ahead to fulfill its greener dreams while smoothly delivering to its international commitments.

Hydrogen Shift and Carbon Credit Market

In line with the current and planned developments, there are also ongoing considerations for hydrogen shift strategy in the near future, as well as carbon market development with formulation of refined regulations, while amending the relevant key pieces from the existing ones.